#2 Ascent Resources - Update thesis (ENG)

Valuation update and summary of the latest press release

On 22/05, the Company published a press release, I include the link below:

Summary of the press release:

On 22 May 2025, Ascent Resources PLC announced a comprehensive package of agreements, including:

i) the conditional acquisition of interests in upstream portfolios in Colorado and Utah,

ii) a GBP1.35 million equity fundraising,

iii) the refinancing of its senior secured debt, and

iv) a series of cost-cutting initiatives and board changes, aimed at advancing its new onshore growth strategy in the United States.

1. Upstream acquisitions

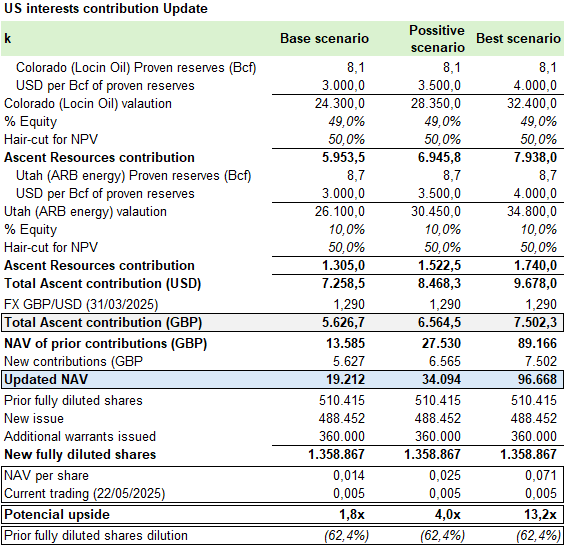

1.1 Colorado interests (Locin Oil)

Acquired interest: 49% stake in over 100,000 acres of oil, gas, and helium leases in western Colorado, with Ascent’s net proved reserves (PDP + PDNP) amounting to 8.06 Bcf of natural gas.

Amount to be paid: USD2,5m

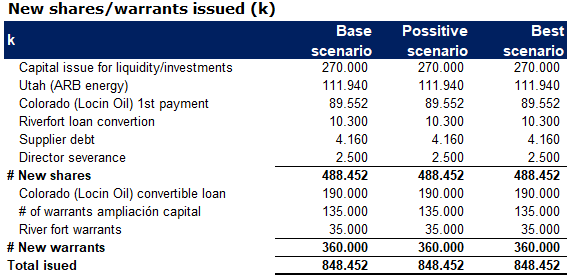

Of which USD600k paid by issue of #89.5m shares at 0.5p per share,

and USD1.9m in a 3-year convertible note with conversion price at 1p (100% premium on the placement price).

Rational:

Immediate access to stable production (#115 wells in production, 2 MMscfd average in 2024 generating USD267k profit) with potential to increase production to 3 MMscfd.

High helium content (up to 1.2%) and additional 663 Bcf step-out prospects with up to 5.3 Bcf of helium.

1.2 Utah interests (ARB Energy)

Initial participation: 10% interest in 80,000 acre concessions in northern Utah, with net PDP reserves of #8.7 Bcf of gas and average production of 2.3 MMscfd in 2024 (earnings of USD496k).

Amount to be paid: USD750k by issue of 111 million shares at GBP0.5p each.

Options and rights:

Right to 50% of incremental production.

Option to acquire an additional 23% for USD1.5m by 15 Oct 2025.

Rights to further drilling (50 % interest).

Rational:

Expands Ascent's footprint in assets with proven reserves and prospective resources (#109 Bcf + #1.3 Bcf of helium).

2. Fundraising and debt restructuring

2.1 Capital increase

Additional issue: GBP1.35m (USD1.8m) by issuing #270m shares at 0.5p (41% discount to previous close) and #1 warrant for every #2 shares at 1p (2 year exercise).

Uso de fondos:

GBP224k for partial cash redemption of senior debt with RiverFort.

Investment in artificial lift technologies in at least six ARB Energy wells.

General corporate and operating costs.

2.2 Refinancing of senior debt

Operation with RiverFort:

Conversion of USD100k principal to #10.3m shares at 0.7245p.

Extension of USD1.05m remaining balance with additional 10% fee and new maturity at 22 April 2027.

Additional scheduled refinancing of USD250k in April 2026 and issuance of additional warrants at 35% of the refinanced debt.

Fixed conversion price at 1p new warrants.

Rational:

Improved maturity profile to align debt payments with cash flow generation from new assets.

Preservation of liquidity in an onshore US investment environment.

3. Changes in the board and cost savings

3.1 Appointment of David Patterson as CEO

Profile: Geologist with 43 years of experience in onshore exploration in the US, former VP Geology at Rose Petroleum.

Condicions: Annual salary of USD120k, of which USD43k will be top-up to joint venture partners; 1p stock option package with 3 year vesting is included.

Rational: Provides key local and technical knowledge to maximise the value of the Colorado and Utah portfolios.

3.2 Departure of Andrew Dennan and board composition

Andrew Dennan will retire after 5 years leading Ascent's transformation and will remain in transition and claims against Slovenia.

Jean-Michel Doublet to take over as Interim-Chairman; review of board composition with a view to appointing a new chairman shortly.

3.3 Cost-saving initiative

Salary reduction: C-suite and directors will reduce their cash remuneration by 30% over the next 6 months and their salary liabilities will be converted into equity at the placement price.

Overall target: 20% annual reduction in general and administrative costs, with savings realisable in the second half of 2025 and beyond.

Valuation update

The Company has brought with this transaction a dilution of approximately 62% to existing shareholders.

Conclusion

The Company's acquisition has been carried at an attractive valuation, giving additional access to increased production and potential discovery of new reserves, where the Company's % interest increases considerably (50% in Utah for newly discovered reserves).

Note that the entire payment for the acquisition of the interests in Colorado and Utah will be made in shares, so the interests in the Company's appreciation of the buyers and sellers should be aligned.

However, at the Company's share price, this transaction has had a very high dilution cost to shareholders (62%).

This is a very large impact, given the Company's downward trend (down 60% YTD25) and unless they know something additional, especially the lead investor, I find it very difficult to understand the very high dilution cost to be borne.

It should be recalled that in Apr-24 and Feb-25 they made a great move with the distribution of 90% of the potential compensation by Slovenia via preference shares. Protecting shareholders' rights with the potential award compensation, as they would not be affected by any dilution.

I include the original thesis where this was explained:

This makes it hard for me to believe that there isn't something else they could be looking at with more information than just investors with the public info they publish.

There is a lot of optionality because of the estimated large undiscovered reserves in the acreage to be acquired, which is in the form of minority interests (49% Colorado and 10% Utah).

In addition, the payment to be made to the holders of the interests in Utah and Colorado will be in shares.

Even more so, when there are #175 million warrants issued in 2023 and 2024, with maturities between 2027 and 2028, and exercise prices above 4.8p per share. These warrants are held by the main shareholder and members of management.

In the issue of the 270 million shares, 1 warrant to convert to 1p in 3 years will also be delivered. The pre-emptive right of issue has been removed, and it will be made to private investors. If this had been done through a public issue, I would probably have bought shares for the warrants, as this would have increased the potential return considerably.

Finally I did not go ahead with the purchase of shares in this company, and for the time being I will continue to watch this stock from the sidelines, awaiting any potential announcement or investment that would give much more asymmetry between risk and reward.

Note that this analysis is not a buy recommendation, but simply an analysis of a Company. In it, I have expressed, in a completely subjective manner, an analysis to read when I need to refresh the reasons that led me to identify potential in buying this Company.